ALJ Regional Holdings (ALJJ) Deep Dive

ALJ Regional Holdings (ALJJ) Deep Dive

ALJ Regional Holdings (NASDAQ: ALJJ) Deep Dive

Investment Thesis

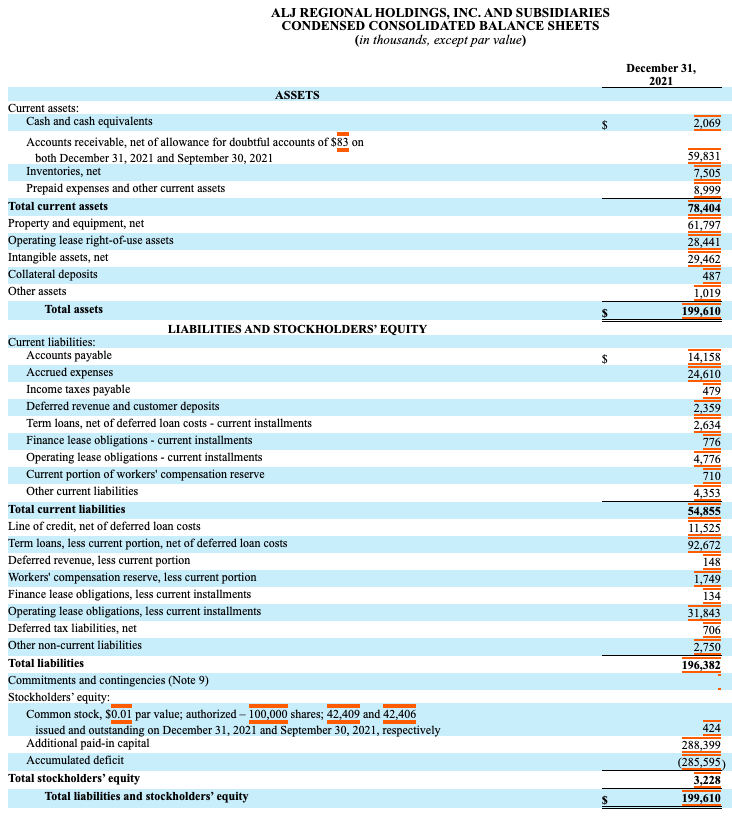

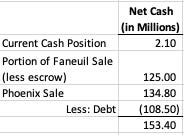

The investment thesis for ALJ Regional Holdings is relatively simple. The company has agreed to sell Phoenix Color Corp. and a significant portion of a company they own called Faneuil Inc. By the end of the 2nd quarter of 2022, both of these transactions are expected to be completed. Once finalized, ALJJ will have a net cash position of $153M and a remaining business that had $87M in revenues for 2021. Essentially, this stock is a risk arbitrage opportunity with a remaining business after the sales finalize. Based on my analysis, I believe the company is currently undervalued by ~ 37%.

Background of the ALJJ

ALJ Regional Holdings Inc. (NASDAQ: ALJJ) is a holding company for two unrelated businesses, Faneuil, Inc and Phoenix Color Corporation. Faneuil provides call center, fulfillment operations, and IT services. Pheonix is a printing business that mainly prints for the publishing industry.

But in reality, ALJ Regional acts like an investment firm or small private equity firm. The majority owner, Mr. Jess M. Ravich (owns over 58% of the shares), has worked in the investment industry in various forms since 1991. You can view a brief bio of him here.

Faneuil

In October 2013, ALJ Holdings acquired Faneuil for $53 million. In 2013, Faneuil was generating around $110 million in yearly revenue and has grown to $325 million in 2021.

On December 22nd, 2021, ALJ Holdings agreed to sell its tolling, transportation, and health benefits portion of Faneuil Inc. for $140M less indemnification escrow of $15M. The deal includes the potential to earn $25M of earn-out payments. The transaction is expected to finalize in the 1st quarter of 2022.

Phoenix

In July of 2015, ALJJ purchased Phoenix Color for $90M. At the time, Phoenix had yearly revenue of $88M which has grown to $115M in 2021.

On February 4th, 2022, ALJJ announced that they agreed to sell 100% of Phoenix Color Corp to Lakeside Book Company for $134.8M (plus or minus $1 million depending on the timing of finalization of the acquisition). The press release states that the transaction is expected to close in the 2nd quarter of 2022.

Commentary/Analysis on Company

ALJJ has a reputation for buying and selling companies for a profit, as shown by the value growth of the transactions above. Additionally, ALJ Regional has purchased other companies that have resold for a profit in the past. In 2005, ALJ purchased Kentucky Electric Steel (which had filed for bankruptcy) for $2.65M and then sold it in 2012 for $112.5M in cash.

Management was friendly to its shareholders after that transaction. In March 2013, ALJ repurchased 30 million shares in a tender offer at $0.84/share when the stock was only trading near $0.40/share, giving shareholders a 100% premium for their shares.

This shows me that ALJ Regional can provide value in the businesses that they purchase and has a history of paying owners after success rather than giving management massive bonuses. Their record of paying shareholders before management is likely because insiders own over 76% of the shares. In this case, management is the owners, and share buybacks effectively pay management by increasing their ownership of the company.

Commentary/Analysis on Current Divestitures

After finalizing the Faneuil and Phoenix transactions, ALJJ will have roughly $274M + $2M (currently on their balance sheet) in cash, with a portion of the Faneuil business still intact.

As shown above, ALJJ has $108.5M in long-term debt; therefore, the company will have a net cash position of $153.4M with the finalization of the two sales. ALJ Regional also currently has a net operating loss carryforward of $135.1M, and therefore these transactions will likely be tax-free.

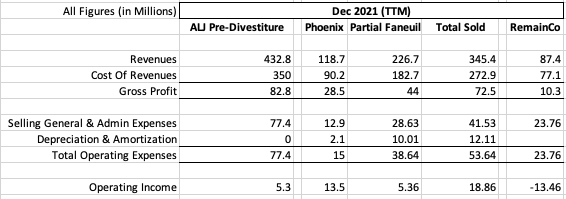

After the Faneuil and Phoenix sales, ALJJ will have a company with $87M in revenues that currently loses money (as shown below).

Note that ‘Partial Faneuil’ represents revenues for the Healthcare and Transportation divisions (~70% of total Faneuil revenues). Due to a lack of information on divisional expenses, I have assumed the costs are also 70% of the total.

A company with $153M in cash plus a remaining business appears to be an attractive investment considering that the market is valuing the stock near $100M. Additionally, as management has a prior history of tender offers after a significant divestiture, I would deem it likely that management could do it again, ensuring a return for shareholders.

But to be sure this is a good investment, let’s perform a more in-depth valuation.

Valuation after Transactions

To value the business (assuming that both sales will finalize), I have performed a Discounted Cash Flow Model (DFC) on the remaining business.

I have valued ALJJ’s stock at about $138M or $3.25/share in my model. Yesterday, the stock closed at $2.38/share, so my model suggests that ALJJ is undervalued by ~37%.

This valuation is heavily reliant on the two sales finalizing because the majority of ALJ’s value is due to the cash to be received by these deals. Because of this, I view this stock like a risk arbitrage opportunity in which I’d expect the stock to trade near my valuation if the deals go through. Currently, the market is handicapping the stock for the likelihood that the sales do not close, hence the 37% spread.

The last point on the above DCF is that my model is imperfect because we (the public) are only subject to limited knowledge from financial statements. Still, I have attempted to build it erroring on the side of conservatism. For example, the company has $30M in lease obligations which I have subtracted from the stocks market value. It is possible that a portion of those leases are the debt of Phoenix or Faneuil and will not be remaining on the books after the sales. There is also limited knowledge on how each individual division has performed and the expectations for the future. Therefore, I built my model with low growth rates and low operating margins.

Risks

One or Both Deals Do Not Close

My investment thesis is based on the assumption that both deals close. If this does not occur, then I would have to revalue the company based on Phoenix and Faneuil’s earning potential.

Ownership

The most significant risk that I perceive is what management will do with the cash once the deals are finalized. The largest shareholder owns over 51% of the stock and therefore can use the cash to his discretion. Based on Mr. Ravich’s background, it is likely that he would purchase another company. In this case, the long-term value of ALJJ would depend on the company he purchases.

A special dividend, tender offer, or stock buyout to take ALJ private are other possibilities that management may consider. A tender offer or buyout would be the best-case scenario for my thesis, as management would likely pay a premium to current trading levels. A special dividend would be a close second as the dividend would likely pay near the stock’s current price.

But as a minority stockholder of this company, this decision is out of our hands, making it a significant risk that needs to be taken into consideration.

Bottom Line

ALJ Regional Holdings is a risk arbitrage-like opportunity with a 37% spread between the current price and the value of ALJ if the two divestitures are finalized.

Thank you for reading! If you have thoughts, questions, or comments on my analysis I encourage you to comment below! The above article is just my thoughts and opinions based on the research that I have performed. If you think that I have missed/overlooked something comment below so we can all learn and make better investment decisions moving forward.