Jerash Holdings (NASDAQ: JRSH) Deep Dive

Jerash Holdings (NASDAQ: JRSH) Deep Dive

Jerash Holdings (NASDAQ: JRSH) Deep Dive

Welcome to the Dark Side of the Street! Here we shed light on the dark corners of the market. If you haven’t already, sign up here for weekly updates or share with your friends and family. If you’re new to special situations, see some of my learning resources on my substack home page to learn more! Feel free to reach out with any feedback.

Disclaimer: Nothing on this newsletter or on this blog is investing or financial advice; please see our full disclaimer here.

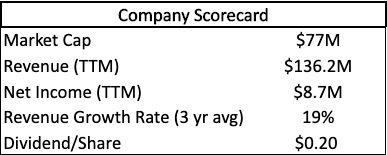

In a competitive market such as the stock market, it can be hard to gain an edge on the market. But I believe that I have found a gem on the Dark Side of the Street. This stock has some rare qualities that are unusual to find. It is a value stock with low financial risk and is a growing company that pays a small dividend. Essentially, everything that one would want in an investment. But as the stock market is so competitive, hitting this quadfecta is rare and makes me think... am I really the only person who has stumbled upon this company? I know this is a company with a market cap of only $77 million, but why aren’t all small funds in on this pushing the company to a more reasonable valuation? I’m skeptical, to say the least. I also don’t have a ton of knowledge about this industry and could be missing or overlooking something. Therefore, I have decided to make a series on this company, with this article being Part 1. In this post, I’ll describe why this stock catches my eye and what questions I still have after this initial dive. Because sometimes, in the stock market, the most significant risk people are taking on is a lack of knowledge or understanding. A stock could look incredibly cheap with minimal risk if you have an extensive knowledge gap. So, you believe that your risk is low when you are taking on a ton of risk. If we can clear that hurdle, we may understand why the market undervalues this company.

So, without further ado, let’s dive into Jerash Holdings.

Company Background

Jerash Holdings (NASDAQ: JRSH) is an apparel manufacturer for known brands such as Adidas, New Balance, The North Face, and others. The company operates factories mainly in Jordan and then exports products to these big brands. JRSH has most of its sales in the United States, with about 10% of its sales coming from Jordan and other parts of the world.

Investment Thesis

As I stated in the intro, the investment thesis for Jerash is simple. It’s just a good company with good metrics such as a high revenue growth rate, a paying dividend, and a solid balance sheet with low financial risk. Plus, the stock is trading at a reasonable price.

Balance Sheet

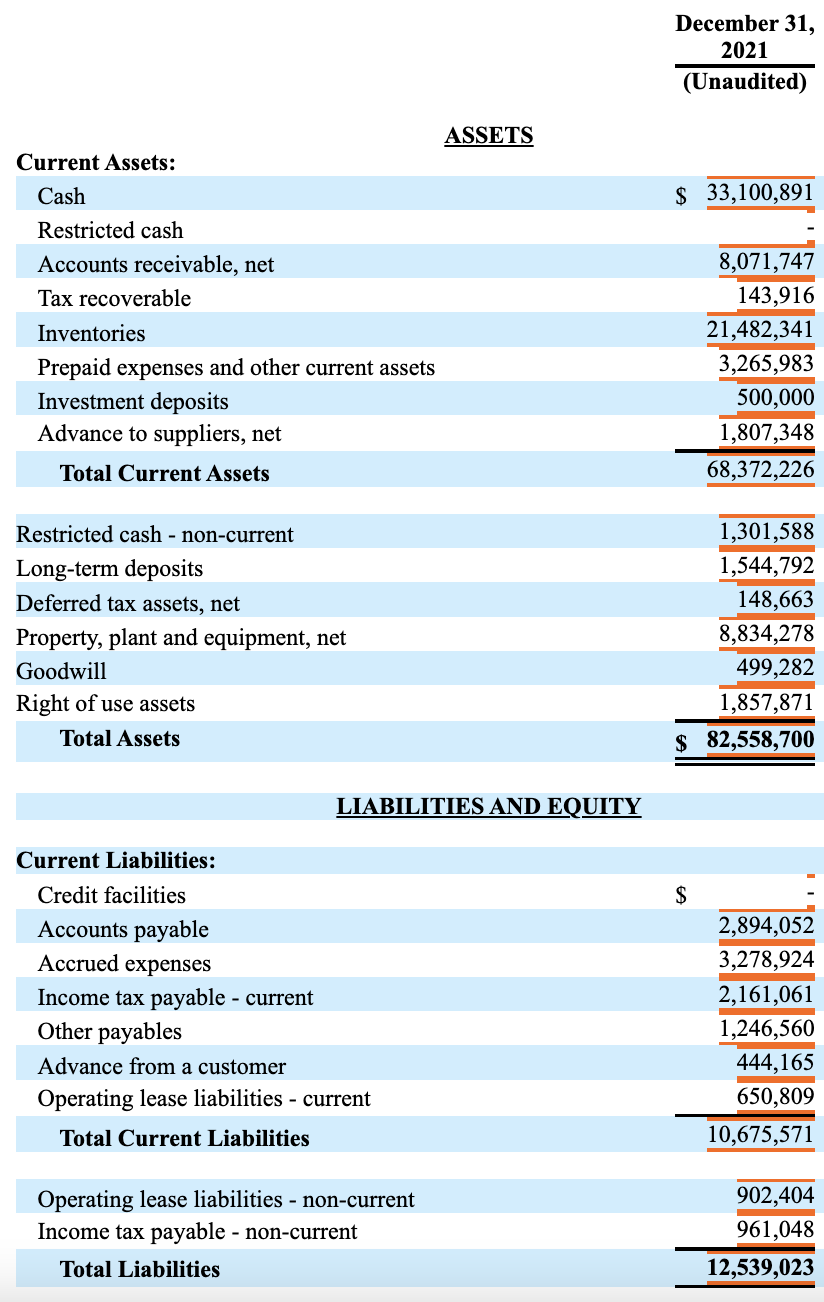

As shown below, Jerash is cash heavy, with about 40% of its assets held in cash or cash equivalents. One of the interesting things about this company's cash position is that the company does not hold much long-term debt. JRSH has ~ $1.5 million in capital leases for its production facilities. But other than that, the cash position has not been funded by debt. In October of 2021, Jerash made a stock offering of 1 million shares and received $6.25 million from the offering. But even without the funding from that offering, the company still has about 32% of its assets held in cash.

Source: JRSH’s December 31, 2021, 10-Q

A heavy cash position can be a double-edged sword. On the one hand, it shows the company has a history of generating solid free cash flow and could survive in extreme cases, thus financially de-risking the company. On the other hand, the company has not put this capital to work, which could fuel growth. Therefore, as an investor, we would like to see a more significant dividend paid out if the cash is not necessary to fund the business or create growth.

In this case, Jerash is building a new production facility so investors should expect the company to grow.

Income Statement

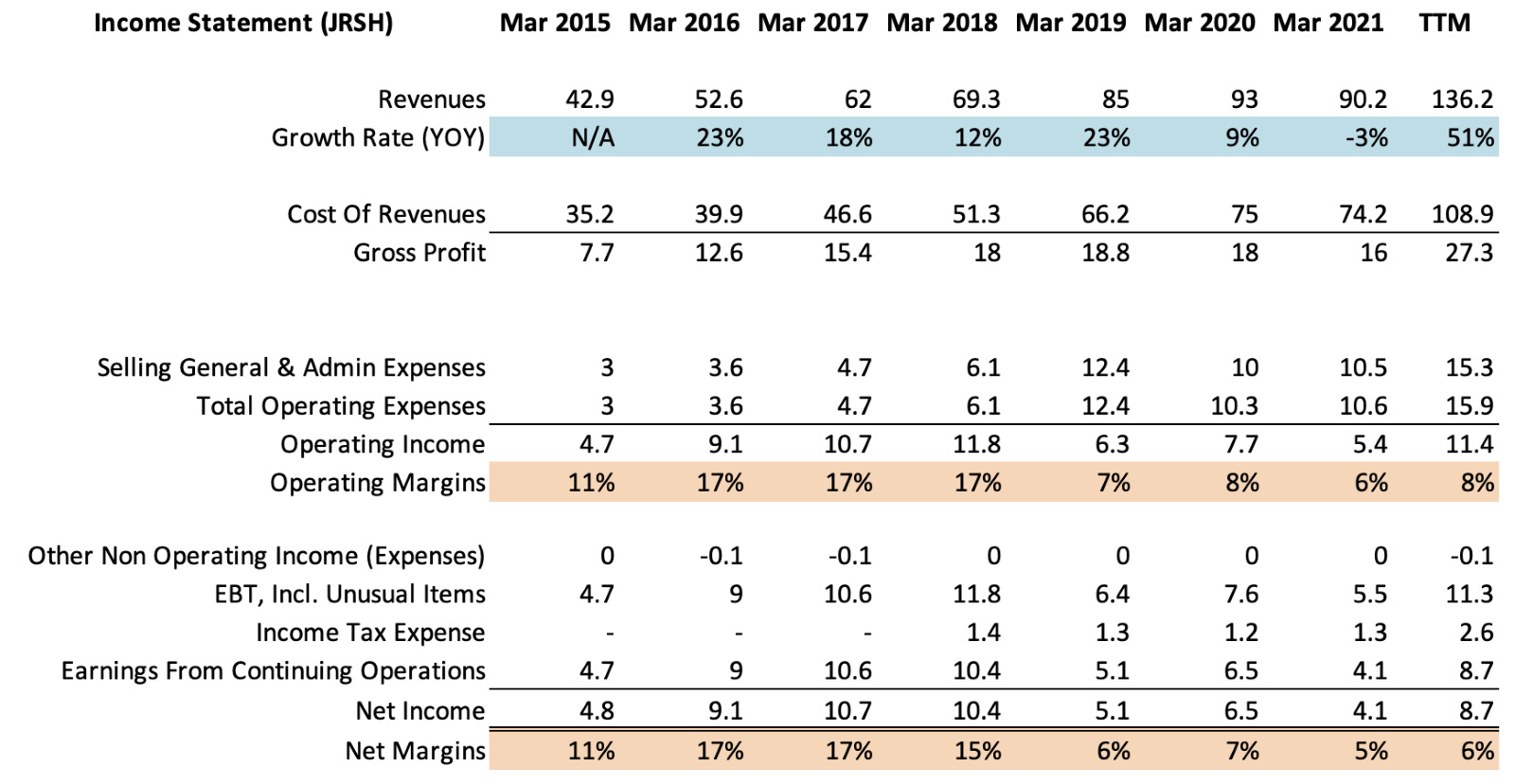

Source: Data Obtained from Seeking Alpha

When I evaluate Jerash's income statement, what sticks out right away is the revenue growth (especially recently). JRSH has increased its total revenue by 50% in the past year. And if you're skeptical of the trailing 12-month figures, don't worry; they are accurate to the company's expectations. According to the December 2021 investor presentation, management is projecting about $141 million in total revenue.

The company’s operating income does lag the apparel industry by about 6%. This low operating income gives me some hesitation especially considering that between 2015 and 2018, the company had significantly higher efficiency. All of this has me asking more questions than providing answers. Why such a massive drop-off in margins? What margins can we expect moving forward? Was this due to having production facilities not operating at capacity or just new facilities that needed time to ramp up production? So many questions, not enough easy answers.

Dividend

Jerash Holdings also currently pays a $0.20/share dividend. This dividend is a payout ratio of roughly 25%. In my opinion, this is a reasonable amount, especially considering that the company is currently expanding. The company has a history of paying sizable dividends, at times paying out 50% of earnings. So, it would not surprise me if JRSH decides to increase its dividend. But that’s just my speculation.

Valuation

Usually, I like to perform discounted cash flow (DCF) analysis to value a company. But embedded in a DCF are many assumptions of what the future holds for a company. And as I stated before, I still have many questions about the future of the company/industry moving forward (see specific questions in the risk section below). Therefore, I will perform a simple comparative analysis to determine a rough price estimate for the stock.

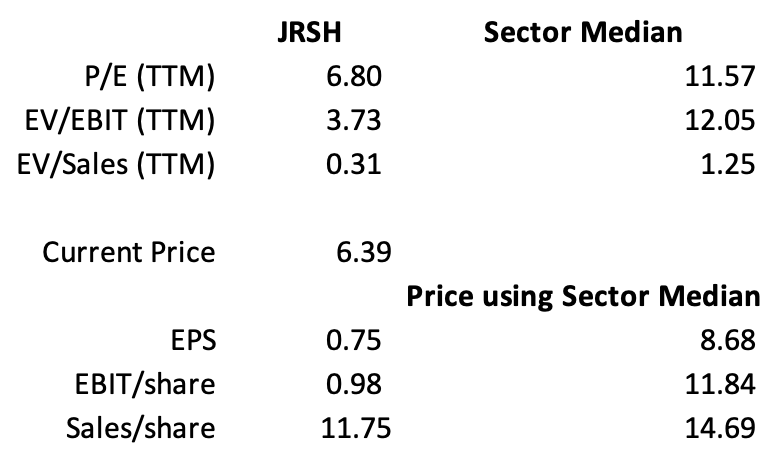

Source: Data obtained from Seeking Alpha

JRSH's stock price indicates that it is cheap no matter how you slice the data. Above we can see that if the company traded at industry medians the company should trade between approximately $8.50 - $15/share.

The larger question that I hope to answer in Jerash Holdings Deep Dive Part 2 is if the current discount by the market is justified. The current financial statements indicate that this stock should be trading at a higher valuation, but maybe there is more to JRSH that I’m missing.

Risks

Jerash Holdings has low financial risk as the company has little debt. But it suffers from one significant risk common with micro-cap stocks: customer and supplier concentration risk. JRSH has two customers which make up 91% of their total revenue. And the company obtains 30% of its materials from 2 suppliers. I am mainly concerned with the lack of diversification in customers. 91% from two customers is incredibly high, especially considering that the #1 customer accounts for 68% of the total. Essentially all the company's growth has come from 1 customer. In general, growth is excellent, but obviously, if that account is lost, JRSH will lose significant revenues in the short term and need to scramble to find another customer as they are currently spending money creating another production facility.

The second risk I perceive is the location of their facilities. Jordan is in the Middle East located at the heart of some politically unstable countries (Saudi Arabia, Iraq, Syria, etc.). If the political environment changes for the worse in any of these countries, Jerash could be negatively affected, to say the least.

Lastly, we have the overall economic landscape to think about regarding the risk of Jerash. We are currently in an inflationary environment, so how will that affect Jerash. Generally, companies that have pricing power perform well compared to peers. But in this case, this is unlikely with such a small company with large brands as customers. For now, I'll deem this a significant risk for this company, but I hope to dive deeper into this in Part 2.

More Questions to Answer in Part 2

In addition to understanding this industry better, here are some company-specific questions I hope to answer.

In general, how sustainable is the current growth rate?

Will Jerash be able to gain more customer contracts? (And hopefully diversify their customer base, maybe kill two birds with one stone?)

What about Jerash’s direct competitors? How do they stack up against other companies manufacturing the same brands as JRSH?

In general, does Jerash Holdings have a competitive advantage?

Bottom Line

Jerash Holdings has the appearance of a growing value stock which has a significant net cash position and currently pays a fair dividend. In Part 2 of this series, I hope to uncover more specifics about this company to perform a DCF properly.

Thank you all for reading! See you next time on the Dark Side!