Kyndryl Holdings (NYSE: KD) Deep Dive

Kyndryl Holdings (NYSE: KD) Deep Dive

Kyndryl Holdings (NYSE: KD) Deep Dive

Welcome to the Dark Side of the Street! Here we shed light on the dark corners of the market. If you haven’t already, sign up here for weekly updates or share with your friends and family. If you’re new to special situations, see some of my learning resources on my substack home page to learn more! Feel free to reach out with any feedback.

Disclaimer: Nothing on this newsletter or on this blog is investing or financial advice; please see our full disclaimer here.

“I’m so good that I’m so bad”

-Eminem

Kyndryl is an interesting stock that is possibly so bad that it’s good. The company was formed from a recent spinoff from IBM as Big Blue attempted to eliminate non-growth divisions of their company. So essentially, KD is in a non-growing business that lost money for IBM and hurt their overall earnings. Obviously an incredibly attractive investment opportunity, right? But hey, it wouldn’t be on the Dark Side if it was a great business in which the consensus was extremely positive (you know what you signed up for here). Let’s dive into the actual company.

The company is in the IT infrastructure services industry, providing consulting and other services to many of the top companies in the world. And oddly enough, the largest business of its kind currently doing about $18 billion in total sales. At this point, I feel the need to be honest and state that I’m not an expert in this industry and only have a general understanding of the services that this company provides to its clients. In this case, I don’t think that I must be an expert to realize that this company is trading incredibly cheap. For more detail on Kyndryl’s services, I’ll outsource the generals to their latest investor presentation below.

This is a turnaround company in which I feel that the market is building in a doomsday scenario and I’m just not as gloomy as the consensus.

Kyndryl Story

Typically, I’m a fairly ‘show me the numbers’ type of investor. I like to see it before I bet on it. But this is more of a qualitative position that, if correct, should provide a risk-adjusted return. So, here’s the idea/story.

Kyndryl was a money-losing division for IBM before the spinoff in October of 2021. IBM was okay with the division losing money as they wanted to upsell clients for their other products and services. AKA- losing money for this division was fine as long as it provided more business (at higher margins) for their other divisions. This strategy was obviously no longer working, hence the spinoff.

As a part of IBM, the market that Kyndryl could operate in was limited as they wanted each client to move all their business to IBM. Now that the companies are separate, the potential market for Kyndryl has increased dramatically from $240B to $510B (estimated from KD management).

As an independent company, Kyndryl will have the ability to decide who its clients will be and raise its operating margins to turn a profit. The business is also likely necessary for large businesses that aren’t tech-savvy but still need to operate in the cloud or need help with the tech side of their company. As Kyndryl is already massive compared to all competitors, they are uniquely qualified to take this business

Investment Thesis

Kyndryl should be worth dramatically more if they can complete a turnaround in which they eliminate unprofitable clients and cut unnecessary costs. Plus, the spinoff from IBM allows KD to attack a previously untapped market, enabling them to increase revenues.

The Noise and Turnaround

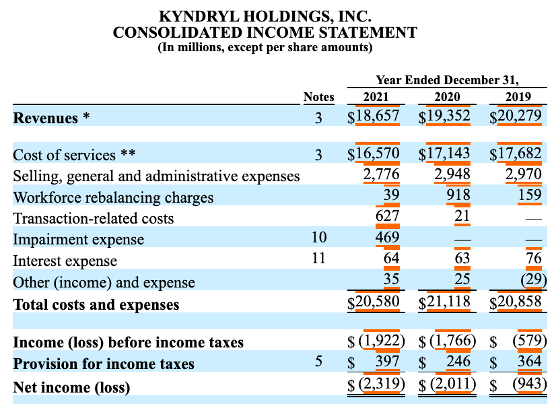

Since the spin-off in October of 2021, there has been a lot of noise surrounding this company. Their first quarterly report stated that they lost almost $700M in Q3 2021, and their annual filing for 2021 shows that they lost $2.3B for the year. Additionally, revenue was down by almost $1B for the third consecutive year. Obviously, not great, and at that rate, the company should be getting ready to file the bankruptcy papers.

Fortunately, there is a decent amount of accounting write-offs lumped into one year plus one-time spinoff costs embedded within these figures. So, the bankruptcy lawyers don’t have to worry just yet about Kyndryl.

As shown above, there were about $1B in losses related to impairment expenses and transaction-related costs (spinoff costs). These are non-recurring expenses, so the company only has about a billion in reoccurring losses (still terrible, but a bit better right?).

Well, the point is that the company needs to reign in its costs. Kyndryl knows this and has provided us some guidance for why their margins are so terrible.

According to the graphic above, 40% of their business is terrible and losing money. If I were to guess, these are the clients that were supposed to provide IBM additional revenues from products/services in other divisions. According to the latest earnings call, the current strategy is to upsell the ‘bad’ clients or let them go. As the company is guiding for ~$16B in earnings for 2022, letting them go appears to be the main solution.

The second part of the strategy is to sign new clients previously disallowed by them as a part of IBM. The company has already announced partnerships with Microsoft Cloud, Google Cloud, AWS, and others. This will allow the company to sign new clients using these applications (prior, they were only allowed to take on business for companies using the IBM Cloud or who would convert to their cloud). Kyndryl seems to be on its way to adding new business, but investors should know that signings generally don’t pay off right away. It could be years down the line before we see the revenue from these new accounts.

Positive Indicators

I see a couple of positive indicators for Kyndryl (which may be me reading tea leaves, but at least make me feel better). First, the company recently gained a ~$3B long-term debt at reasonably low-interest rates (Avg. 2.7%). As the creditors are generally incredibly concerned with getting their money back, a low rate does indicate that they feel optimistic about the long-term prospects of KD and that they will be paid.

The second thing is something that always bugged me with this spinoff. IBM kept a 20% in Kyndryl. IBM touted this company as a declining business, and getting rid of it will be great for IBM’s financial statements and yet wanted to keep 20% of the shares. This could mean that IBM has a stronger belief in the business than they marketed to the public.

Valuation

The valuation of this company is genuinely where the bad meets the good in this investment. It’s all about the price we will pay for the possibility of a turnaround. And for the headache and the amount of time this company requires to complete their turnaround, it better be a good return.

Companies with this much uncertainty can be difficult to value, but where the opportunity lies. Because of the uncertainty I’m not going to bang my head against the wall with a full blown DCF and instead keep it simple.

My assumptions are that all $8 billion of their ‘bad’ clients will need to be ‘fired’, and the company will have $10B in reoccurring revenues. I will assume that 25% gross profit margins are attainable with their current client base. And I’m not going to add in any new revenue for the valuation. Additionally, I will use 15% of total revenues for SGA expenses as that has been the historical average for the company. And then, I’ll assume a terminal value of a price/earnings ratio of 10 since this is near the stock market historical average.

If we consider all that, the company should be worth $25.60/share, which is more than double the current share price. And this is what I would consider the dummy-proof model (find unprofitable clients and fire them along with all the expenses related to those clients).

Depending on the potential revenue growth, I believe that there could be further upside to this company, but at this point hard to quantify. But for now, I’m comfortable with the risk on the dummy-proof model as that seems to be a relatively simple plan to execute.

Risks

The largest risk we are taking on is that the turnaround is executed properly. Costs need to be reigned in within a timely period. If that is not possible then this entire thesis crumbles. But as stated above at the current stock price, I believe that this risk is worth taking.

Another risk is the general decline in revenues for Kyndryl. This is concerning as it could indicate a lack of demand for this service, in which case overcoming that battle is a significant headwind that could derail a turnaround.

In conjunction with the above risk is my general lack of industry knowledge. As I stated previously, I’m not an expert in the industry, I could be totally off in with the idea that $10 billion of revenues is the market for this company. And if the company cannot at least stabilize revenues or quickly reign in losses this company could be in significant trouble.

Bottom Line

Kyndryl is a turnaround stock that can double an investor's money if the company can execute its current cost-cutting strategy.

Disclosure: I own shares of KD

PS: Here’s the Eminem song from the quote in the beginning!

Thank you all for reading! See you next time on the Dark Side!

Hey Matt,

I guess you were a bit early.

Recently insiders including CEO & CFO have purchased shares, as well as David Einhorn (Greenlight Capital) and IBM has exited their position completely, which I see as a positive as selling pressure should subside.

At the same time results from AAA-Initiatives aren't really showing up in the numbers yet, the management is talking a lot about Adjusted figures (and not really cash flows), and finally there is this lawsuit with $1.6B potential liability connected to AT&T and work done by Kyndryl (before Spin), which is hard to assess.

Do you have any updated thoughts on KD?

Cheers